Tulsa gets overlooked. People fixate on Austin, Nashville, Phoenix — and meanwhile, one of the most affordable, livable, and genuinely smart places to buy a home in America keeps quietly appreciating. If you're seriously considering buying in Tulsa in 2026, this guide is the breakdown you actually need: real numbers, real zip codes, real school data, and a clear answer on the $450K vs $740K decision.

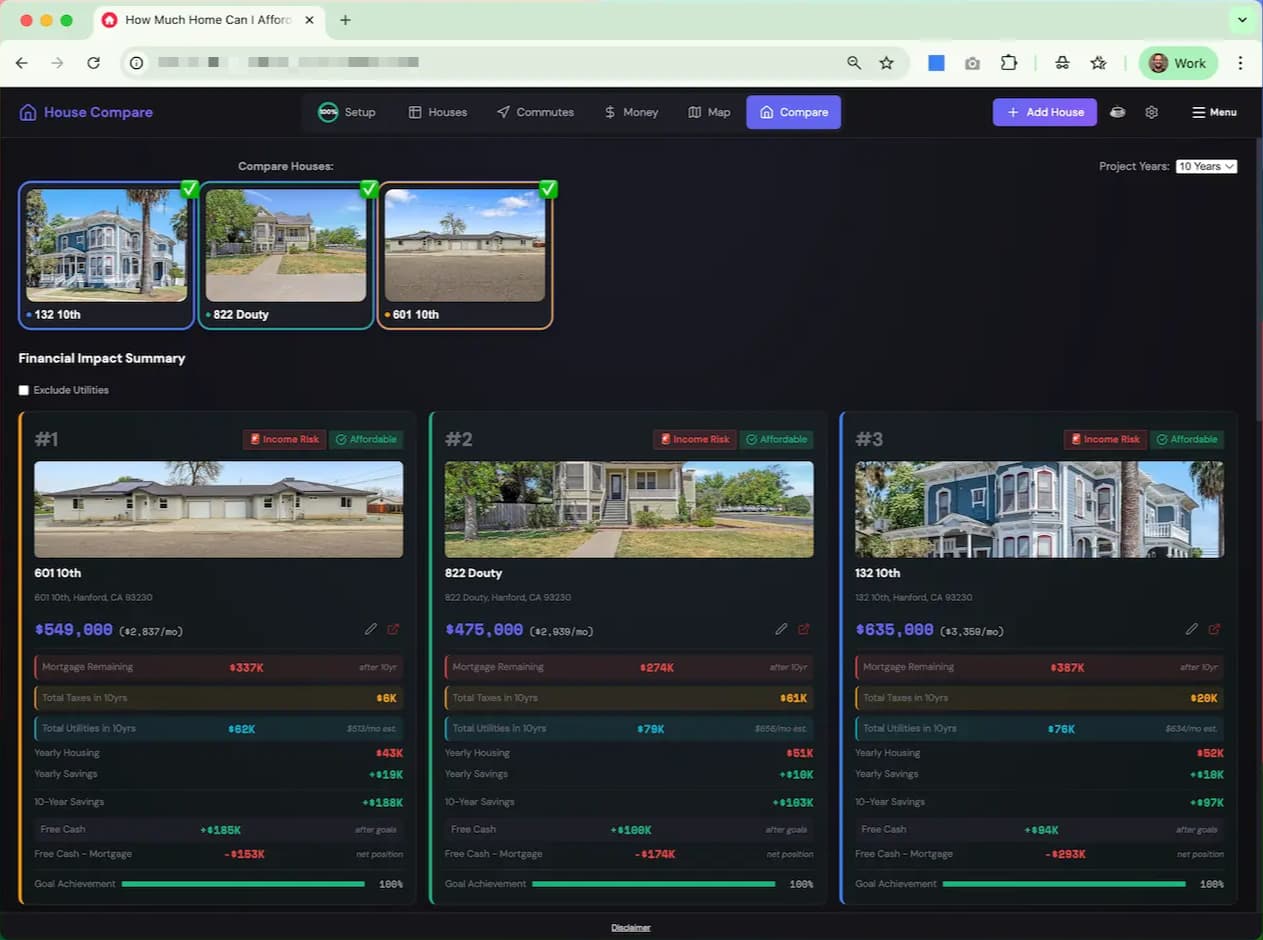

Before you decide on a house, make sure you know your real number — not just the bank's number. Try the How Much House Can You Afford tool to compare Tulsa homes side-by-side against your actual income and life goals.

The Tulsa Market in 2026 — Snapshot

Tulsa is a stable, mid-sized market that's been quietly outperforming expectations. Here's where things stand as of early 2026:

- Median metro home price: ~$248,500 (up 4.3% year-over-year)

- Average days on market: 36–41 days

- Inventory: ~2.0 months supply — technically a seller's market

- Mortgage rate environment: ~6.5%

- 5-year cumulative appreciation: ~55% across the metro

That 55% five-year figure is the headline most people miss. Tulsa isn't a stagnant rust-belt market. It's been quietly building wealth for homeowners who bought smart.

Property Taxes: The Good News

Oklahoma is one of the most homeowner-friendly states in the country when it comes to property taxes — and Tulsa County specifically is low even by Oklahoma standards.

- Effective rate: ~1.06% of assessed value

- Homestead exemption savings: $91–$142/year (primary residence)

| Purchase Price | Est. Annual Tax | Monthly Tax Cost |

|---|---|---|

| $350,000 | ~$3,710 | ~$309 |

| $450,000 | ~$4,770 | ~$398 |

| $550,000 | ~$5,830 | ~$486 |

| $740,000 | ~$7,844 | ~$654 |

Property taxes are not a dealbreaker in Tulsa at any of these price points. The $256/month difference in taxes between a $450K and $740K home is real money, but it doesn't change the fundamental decision. What changes the fundamental decision is the resale market — more on that below.

Best Zip Codes in Tulsa (Ranked)

Not all Tulsa zip codes are created equal. The difference between 74137 and 74106 isn't just price — it's schools, crime rates, appreciation trajectory, and how easily you'll be able to resell. Here's the honest ranking:

| Rank | Zip | Area | School Grade | Median Home Value | Notes |

|---|---|---|---|---|---|

| #1 | 74137 | South Tulsa / Jenks border | A+ | $384,500 | Best overall; Jenks & Union schools |

| #2 | 74037 | Jenks | A+ | $350K–$400K | #1 ranked suburb in Tulsa County |

| #3 | 74133 | South Tulsa | A+ | $220K–$353K | Most affordable A+ entry point |

| #4 | 74008 | Bixby | A | ~$426,000 | Fast growth, newer homes, strong schools |

| Honorable | 74114 | Midtown Tulsa | A+ overall / B schools | Higher per sq ft | Character homes, walkable, Brookside/Cherry St |

Avoid: 74105 (higher crime, C-rated schools) and most of 74106 (bottom 50% of Oklahoma public schools). These zip codes are cheaper for a reason — and that reason will follow you to your resale.

Best Public Schools in Tulsa

This is where Tulsa requires a critical distinction: Tulsa Public Schools (TPS) are not the same as the suburban districts that overlap with Tulsa zip codes. TPS as a whole underperforms the state average significantly — 14% math proficiency vs. 25% state average. The top schools are in suburban districts:

- Jenks Public Schools (74037 / 74137) — Consistently top-ranked in Oklahoma. Jenks High School: Grade A. One of the most sought-after school districts in the state.

- Union Public Schools (74133 / 74137) — Large, highly rated district. Union High School: Grade A. Serves much of south Tulsa.

- Bixby Public Schools (74008) — Rapidly growing, strong ratings, newer facilities. Grade A.

- Broken Arrow Public Schools (74011 / 74014) — Grade A, large and well-resourced. More affordable entry points than Jenks or Bixby.

"If schools matter to you — and they should, because they'll matter to your buyer in 5 years — buy in Jenks, Union, Bixby, or Broken Arrow districts. Full stop."

The good news: the best school districts align perfectly with the best zip codes for appreciation. You're not choosing between schools and investment return — you're choosing both together.

Who Can Actually Afford What in Tulsa

Here's where most home-buying advice fails you. Lenders will tell you what you qualify for — which assumes you have no other financial goals, never travel, and don't mind maxing out your housing ratio. That's not real affordability. Here's what the numbers actually look like at 6.5%, 30-year fixed, 20% down, with standard 28% front-end DTI:

| Price | Down (20%) | Monthly P+I | +Tax+Ins | Income Needed |

|---|---|---|---|---|

| $250,000 | $50,000 | $1,264 | ~$1,600/mo | ~$68,500/yr |

| $350,000 | $70,000 | $1,770 | ~$2,230/mo | ~$95,500/yr |

| $450,000 | $90,000 | $2,275 | ~$2,850/mo | ~$122,000/yr |

| $550,000 | $110,000 | $2,781 | ~$3,450/mo | ~$147,900/yr |

| $740,000 | $148,000 | $3,742 | ~$4,600/mo | ~$197,000/yr |

The Tulsa metro median household income is about $60,000/year. Even in the top zip codes (74137, median: $103,963), the buyer pool narrows dramatically above $450K and becomes genuinely thin above $600K. This matters enormously for resale.

- Range where most buyers can realistically buy: $220K–$370K

- Range where homes sell fastest: $250K–$400K (sub-2 week close in good condition)

- $450K+: Buyer pool shrinks significantly; requires top 15% of Tulsa incomes

- $740K+: Buyer pool is thin — likely under 5% of metro households can qualify

The Core Question: $450K vs $740K for a 5-Year Resale

Let's be direct. Both are valid purchases — but they carry very different risk profiles if you're planning to sell within 5 years and need to at least break even.

The $450K Case

What you get: In 74137 or Bixby, $450K gets you a solid 2,200–3,000+ sq ft home in a top school district. It's above the entry-level frenzy, but still within reach of a meaningful buyer pool.

The math over 5 years: At a conservative 3.5%/year appreciation in these zip codes:

- Year 5 estimated value: ~$533,000–$545,000

- Equity after 5 years (appreciation + principal paydown): ~$160,000–$175,000

- Homes at this price in 74137/74008 sell in 30–45 days

- Break-even risk: Low

The resale reality: When you go to sell, the household income required to buy your $533K resale home is ~$134K. In the 74137 zip code where the median income is ~$104K, that's tight but achievable. You'll have buyers.

The $740K Case

What you get: Luxury quality — larger lot, premium finishes, potentially a custom or semi-custom build. In Tulsa terms, you are now in the top 3–5% of all home sales.

The math over 5 years: At 3.5%/year (being optimistic for the luxury segment):

- Year 5 estimated value: ~$876,000–$900,000

- On paper, that looks great. The problem is getting there.

The resale reality: To buy your $880K resale home, the buyer needs to earn ~$197K/year and come up with $176K in cash for a down payment. In Tulsa, that buyer pool is extremely small — likely a few hundred qualified households actively looking at any given time. This means:

- Homes at this price sit 60–90+ days on market (vs. 36 for median)

- Buyers at this tier are sophisticated and negotiate hard

- If the market softens even 5–8%, you may not break even after 5–6% agent commissions

- Break-even risk: Moderate-to-High on a 5-year timeline

Bottom line: $740K in Tulsa is not wrong if you plan to stay 10+ years. But for a 5-year break-even horizon, the thin buyer pool is a real and significant risk. Tulsa is not a tier-1 luxury market — $740K competes against a very small, very selective pool of buyers.

Age of Home: The Sweet Spot

The question of which era of construction to target is one most buyers don't ask carefully enough. Here's the honest breakdown for Tulsa:

| Era Built | Assessment |

|---|---|

| Pre-1980 | High risk — foundation concerns, outdated plumbing/electrical, possible lead paint. Avoid unless fully renovated and priced accordingly. |

| 1980–1994 | Moderate risk — major systems (HVAC, roof, plumbing) are at or near end of life. Budget for replacements soon. |

| 1995–2010 ✓ Sweet Spot | Modern construction codes. Past initial depreciation. Predictable system timelines — you know when the roof, HVAC, and water heater will need replacing. Neighborhoods are established. Often updated already. |

| 2010–2018 | Good — lower maintenance risk, but you're paying a new-ish construction premium. Less negotiating room. |

| 2019–Present | New construction premium — maximum price, least negotiating leverage, some areas still developing infrastructure (traffic, retail, etc.). |

The best buy in Tulsa: a 2000–2012 built home in an established neighborhood. At this age, major systems are predictable — you can plan for a roof in 5–7 years, an HVAC in 3–5, rather than inheriting emergencies. In Jenks, Bixby, and South Tulsa, this era lands naturally in the $380K–$520K range. That is not a coincidence — it's the market working correctly.

The Full Comparison: $450K vs $740K vs The Sweet Spot

| Factor | $450K | $740K | Sweet Spot ($420K–$480K) |

|---|---|---|---|

| Buyer pool at resale | Medium-Large | Small | Large |

| Days on market (resale) | 30–50 days | 60–120+ days | 30–50 days |

| Annual appreciation (est.) | 3.5–4.3% | 2.5–3.5% | 3.5–4.3% |

| 5-yr break-even probability | High | Moderate | High (80%+) |

| Property tax/month | ~$398 | ~$654 | ~$370–$440 |

| School access | A / A+ | A / A+ | A / A+ |

| Monthly all-in cost | ~$2,850 | ~$4,600 | ~$2,650–$3,000 |

| Household income needed | ~$122K | ~$197K | ~$115–$128K |

The Sweet Spot: What to Actually Buy

The Recommendation

- Price range: $380,000–$480,000

- Zip code: 74137 (South Tulsa / Jenks border) or 74008 (Bixby)

- School district: Jenks, Union, or Bixby

- Home age: 2000–2012 built

- Size: 2,400–3,200 sq ft

Here's why this specific combination wins:

- You get A+ schools without paying a new-construction premium on a $600K+ new build

- The buyer pool at resale in this range is meaningfully larger than anything above $550K

- Annual appreciation of 3.5–4.5% in 74137 and Bixby is consistent and documented

- A 2000–2012 home gives you predictable maintenance windows — no emergency roof replacement two years in

- Property taxes land at ~$4,000–$5,100/year — very manageable

- Homes in this range in these zip codes sell in 30–45 days — not entry-level chaos, not luxury stagnation

- 5-year break-even probability: very high, assuming no major macro recession

As for the $740K question: it's not irrational, but for a 5-year horizon in Tulsa, you are asking the market to find you a very small, very specific buyer at a premium price. If life circumstances change and you need to sell, the clock on that sale could run 6–12 months at asking price. That's a risk most 5-year plans can't absorb cleanly.

Run Your Specific Numbers

This guide gives you the market context. But your actual decision depends on your income, your goals, your savings rate, and whether you've got plans to travel, start a business, send kids to college, or build real estate as a portfolio. The How Much House tool was built for exactly this kind of decision — paste in your Tulsa listings from Redfin, add your financial picture, and see which house actually aligns with your life over 5, 10, and 30 years.

Ready to run the numbers on your specific Tulsa homes?

Compare Your Tulsa Options →Free. Private. No account needed. Works with Redfin listings.